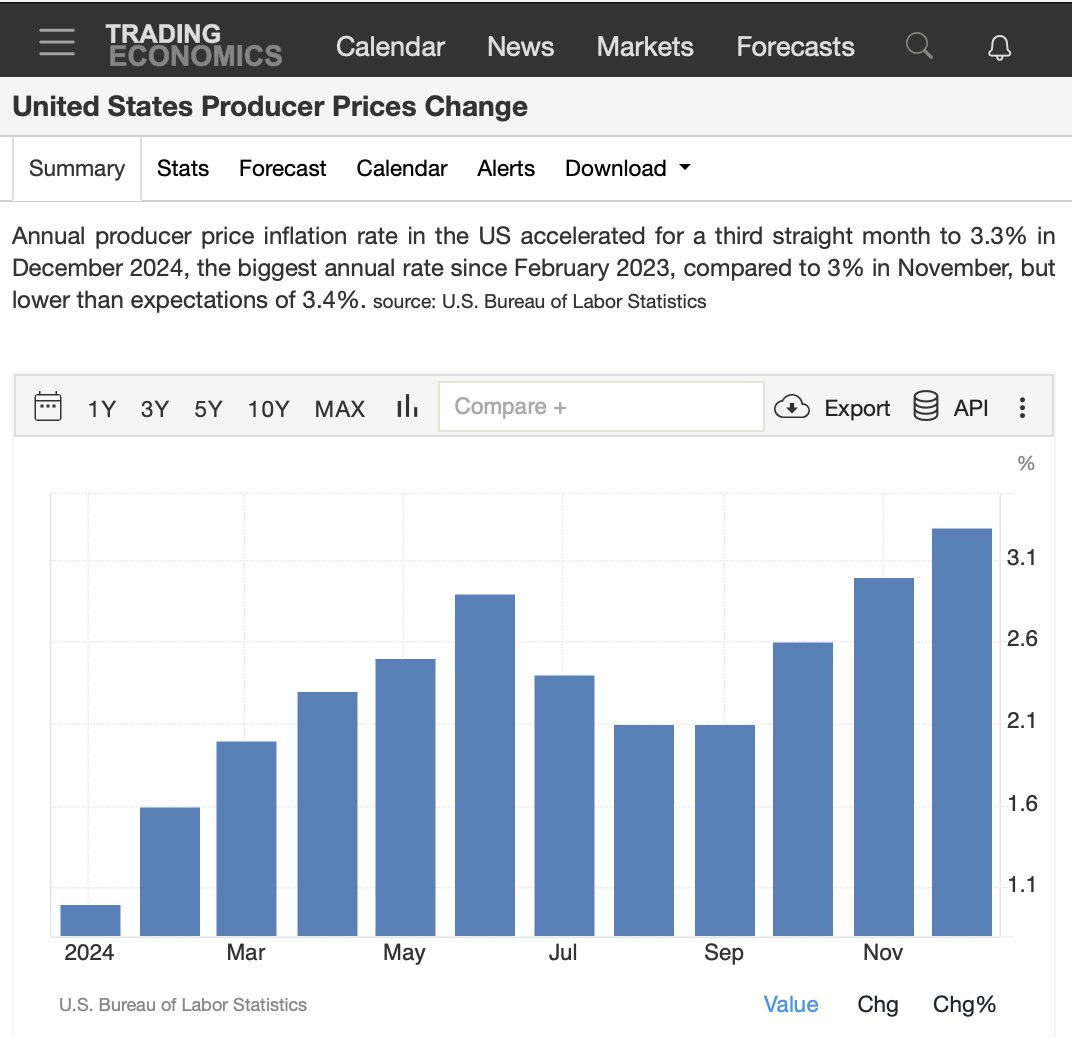

US Producer Value Index (PPI) figures are worse than anticipated.

On a month-to-month foundation, the general PPI rose by 0.2%, under the forecast of 0.4%. Core PPI (excluding unstable objects) remained unchanged at 0.0%, whereas a rise of 0.3% had been anticipated.

On a yearly foundation, total PPI grew by 3.3%, barely under expectations of three.5%. As for core PPI, it rose by 3.5%, additionally under the three.8% forecast.

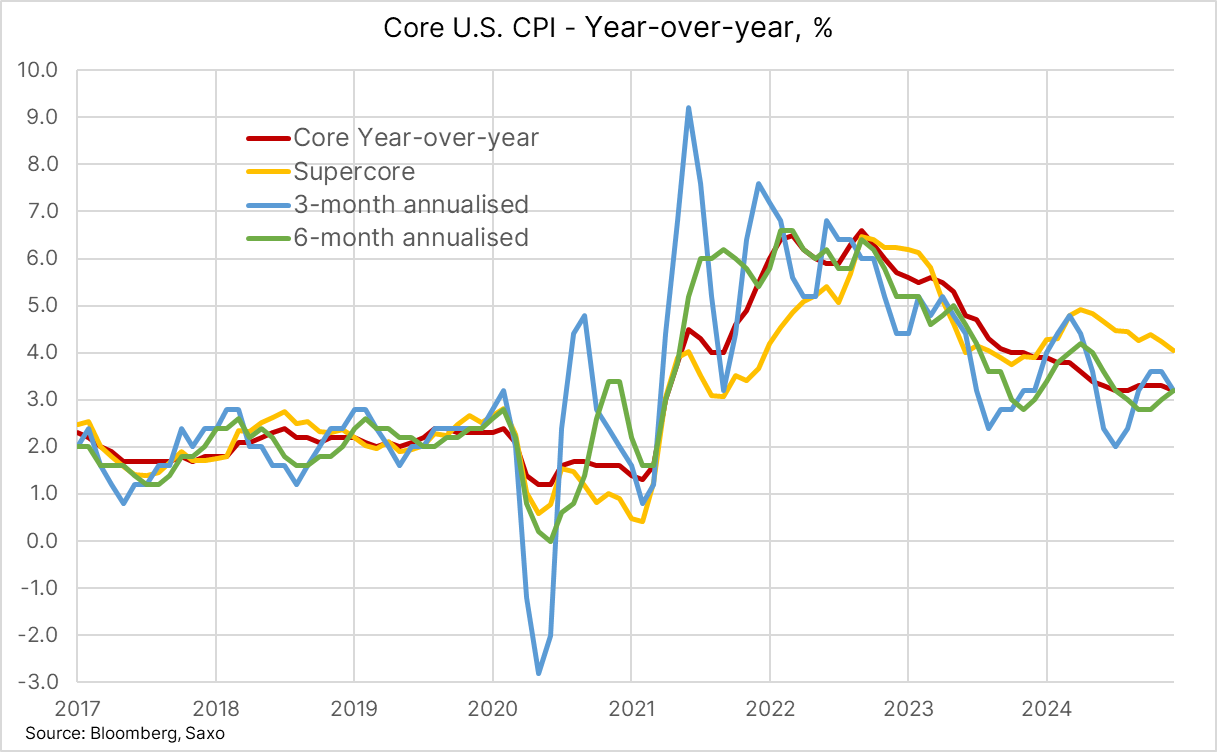

In December, core CPI inflation within the US slowed to three.2% year-on-year, whereas headline CPI inflation reached 2.9% year-on-year, in keeping with expectations. The three- and 6-month annualized charges additionally converged at 3.2%. As well as, supercore inflation fell from 4.25% to 4.05%, signalling a weakening of inflationary pressures in key sectors.

The autumn in inflation stems primarily from decrease power costs, with the worth of oil reaching its lowest degree on the finish of 2024, as a result of fears of an financial slowdown in China. Nevertheless, you will need to level out that because the starting of 2025, the worth of oil per barrel has began to rise once more, which might exert additional upward strain on future inflation indices (CPI):

Inflation is having a very robust impression on sure key sectors: automobile insurance coverage (+11.3%), transport (+7.3%), automobile repairs (+6.2%), metropolis fuel (+4.9%), householders’ prices (+4.8%) and rents (+4.3%).

The housing element, together with rents and proprietor’s equal lease (OER), has now taken over from the power element as the principle driver of rising inflation!

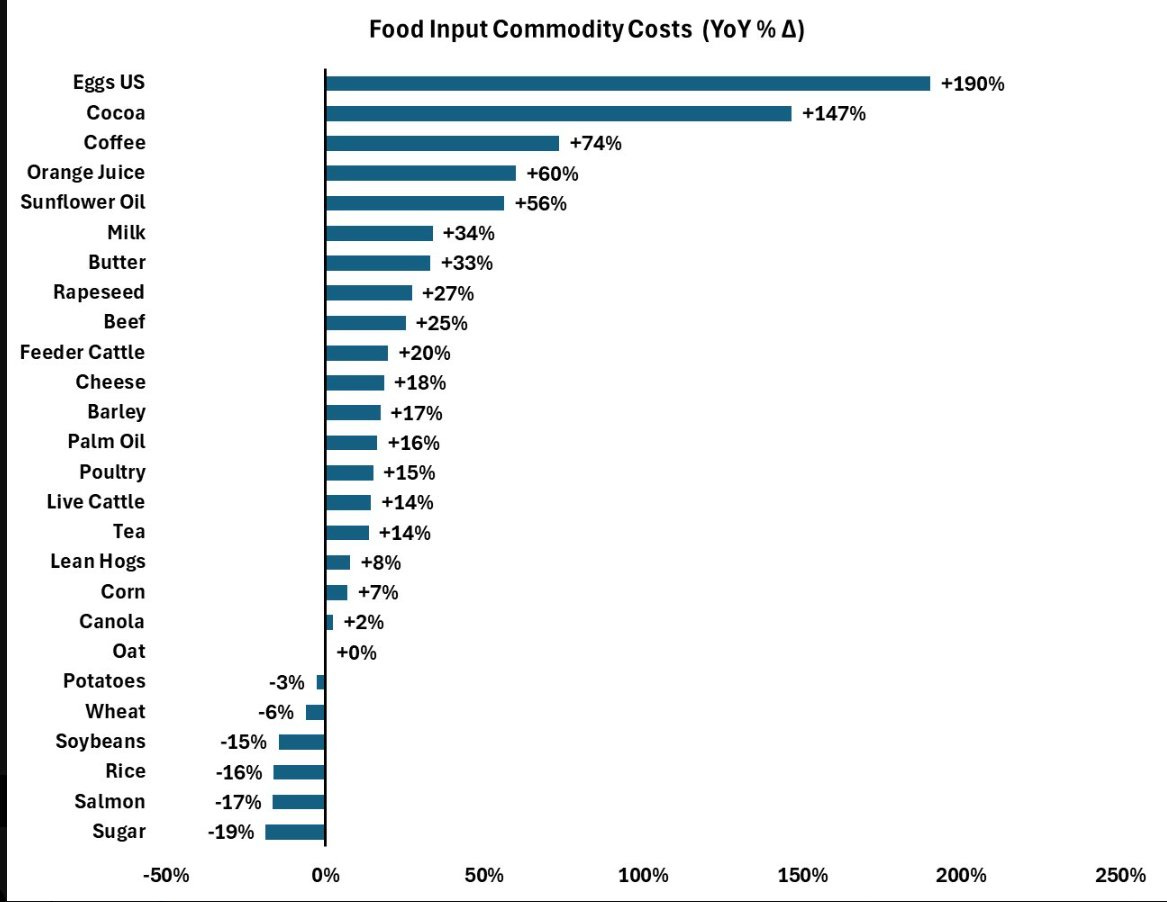

The “meals” element of the index additionally continues to soar, fueled by spectacular rises in agricultural commodity costs:

These information reveal inflationary strain properly under expectations, which, in idea, ought to have a direct impression on the bond market. In precept, a higher fall in inflation ought to result in a sharper discount in rates of interest:

Nevertheless, the bond market faces a brand new risk: inflation is not the one difficulty. The US deficit is now seen as the principle supply of concern.

And for good purpose: the most recent deficit figures are dizzying, revealing a funds state of affairs that continues to deteriorate:

This was the worst begin to a fiscal 12 months on document: spending rose by 10.9%, revenues fell by 2.2%, and the year-to-date deficit jumped by 39.4% to $711 billion.

The US now has an annual deficit of $3 trillion, reflecting a very worrying fiscal state of affairs.

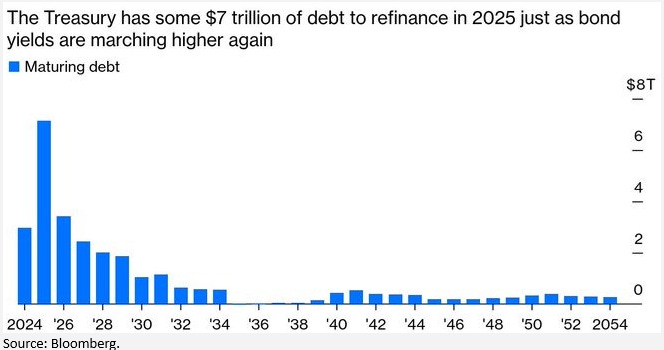

This deficit is available in 2025, a 12 months through which the U.S. will face a veritable wall of debt:

By 2025, the US Treasury might want to refinance round $7 trillion of maturing debt. This monumental quantity coincides with a interval when bond yields are as soon as once more on the rise, additional complicating the state of affairs.

This huge refinancing will result in a major enhance in the price of debt, because the Treasury should borrow at a lot increased charges than when these money owed have been issued. This may mechanically exacerbate the US funds deficit, already at crucial ranges.

As well as, strain of this magnitude on the bond market might result in main tensions. Issuing such a excessive quantity of recent bonds might push buyers to demand much more engaging yields. On the identical time, it might dampen worldwide buyers’ appetites for US debt, accentuating the danger of monetary imbalances.

With such colossal refinancing, the foreign money might depreciate so shortly that even excessive charges is not going to be sufficient to protect the true yield on bond merchandise. That is most likely why the US Treasury bond market is at the moment so unattractive, regardless of the slowdown in inflation.

This refinancing peak in 2025 represents a significant problem for US financial stability, with potential repercussions for international monetary markets. That is exactly the message the bond market is in search of to convey.

Actual yields on US 30-year bonds have fallen again to 2008 ranges. Clearly, bond markets will not be simply involved about inflation. Behind this, a lot broader issues are rising: development at half-tempo, hovering deficits, and maybe even systemic dangers.

This rise in charges represents a threat for the bond portfolios of most monetary establishments.

The colossal losses recorded on the bond portfolios of Major Sellers in the US, amounting to over $364 billion, illustrate the unprecedented strain exerted on the monetary system:

These losses, though at the moment unrealized as a result of technique of holding bonds to maturity, are however profoundly weakening banks’ liquidity.

This is because of a major drop within the collateral worth of those property, which is important for guaranteeing loans and interbank transactions.

With the bond market sounding the alarm, gold is reasserting its conventional function as a safe-haven asset. Buyers, involved in regards to the pressures related to the 2025 debt wall, are turning to gold as a secure asset within the face of rising uncertainty.

This transfer is pushed by fears of a potential devaluation of fiat currencies. When the US Treasury has to refinance trillions of {dollars} of debt at increased rates of interest, budgetary strain might pressure the authorities to undertake expansionary financial or fiscal insurance policies, reminiscent of cash printing or quantitative easing, to soak up this huge debt. These methods are prone to additional weaken the worth of the greenback and different currencies.

In opposition to this backdrop, bodily gold, which isn’t tied to any sovereign entity or financial coverage, is changing into a beautiful asset for buyers wishing to guard their wealth. This anticipation displays a rising distrust of conventional currencies and a need to protect in opposition to the inflationary or devaluation dangers that would accompany the refinancing of this monumental debt.

It is hardly stunning that central banks are turning to gold in such a local weather of uncertainty. In 2024, China formally added 44 tons of gold to its reserves, bringing its whole to 73.29 million fantastic troy ounces in December. This technique is a part of a thought-about strategy to asset diversification, initiated again in 2016 after the election of Donald Trump, and is geared toward securing its reserves within the face of a worldwide surroundings marked by geopolitical and financial instability.

This accumulation of gold can be a part of a method to cut back dependence on the US greenback, in response to the risk to the foreign money’s worth posed by the large refinancing of US debt in 2025. By bolstering its gold reserves, China is anticipating the dangers of a weakening greenback, linked to budgetary pressures and potential financial enlargement wanted to soak up the debt wall. This coverage displays China’s need to guard itself in opposition to international monetary uncertainties and to strengthen its financial autonomy within the face of the greenback’s historic dominance.

🇨🇳 Chinese language reserves for December : 2,280 tonnes https://t.co/MWoAydo5t5 pic.twitter.com/GoYanH1wVx

— GoldBroker (@Goldbroker_com) January 10, 2025

Copy, in entire or partially, is permitted so long as it consists of all of the textual content hyperlinks and a hyperlink again to the unique supply.

The data contained on this article is for info functions solely and doesn’t represent funding recommendation or a suggestion to purchase or promote.