The yr 2025 is starting with stagflation.

In Europe, financial exercise continues its slowdown. The most recent manufacturing PMI indices all present a marked decline, whereas the job market in flip is more likely to be impacted by this slowdown within the months forward.

The German economic system goes by means of a deep disaster that threatens to unfold to Europe and the remainder of the world. In December, the PMI companies index rose modestly to 51.2, suggesting a timid restoration. Nonetheless, the manufacturing sector stays within the midst of a despair, marked by nearly empty order books and a fall in employment for the sixth consecutive month. The service sector, which is intently linked to trade, with 70% of its exercise depending on it, can also be feeling the consequences of the disaster, recording a fall in new orders for the fourth consecutive month.

Job cuts in Germany are on the rise, as corporations search to enhance productiveness to compensate. However larger productiveness means a smaller workforce, additional weakening home demand. Though job cuts stay modest in the meanwhile, the present financial fragility factors to a potential deterioration.

In Europe, the eurozone economic system recorded a downturn in December, marked by a fall in manufacturing employment and a decline so as books since April 2023.

In america, related tendencies are rising: manufacturing facility orders fell by -0.4% in November, following a year-on-year decline of -1.9%, representing the sharpest contraction since June. New orders for sturdy items fell by -6.4% year-on-year, whereas unemployment claims are rising steadily, reflecting the rising fragility of the labor market. On the similar time, consumption is slowing down because of excessive costs, and retail gross sales are displaying indicators of weak point.

With inflation persisting, unemployment rising and industrial order books emptying, a worldwide recession seems more and more doubtless.

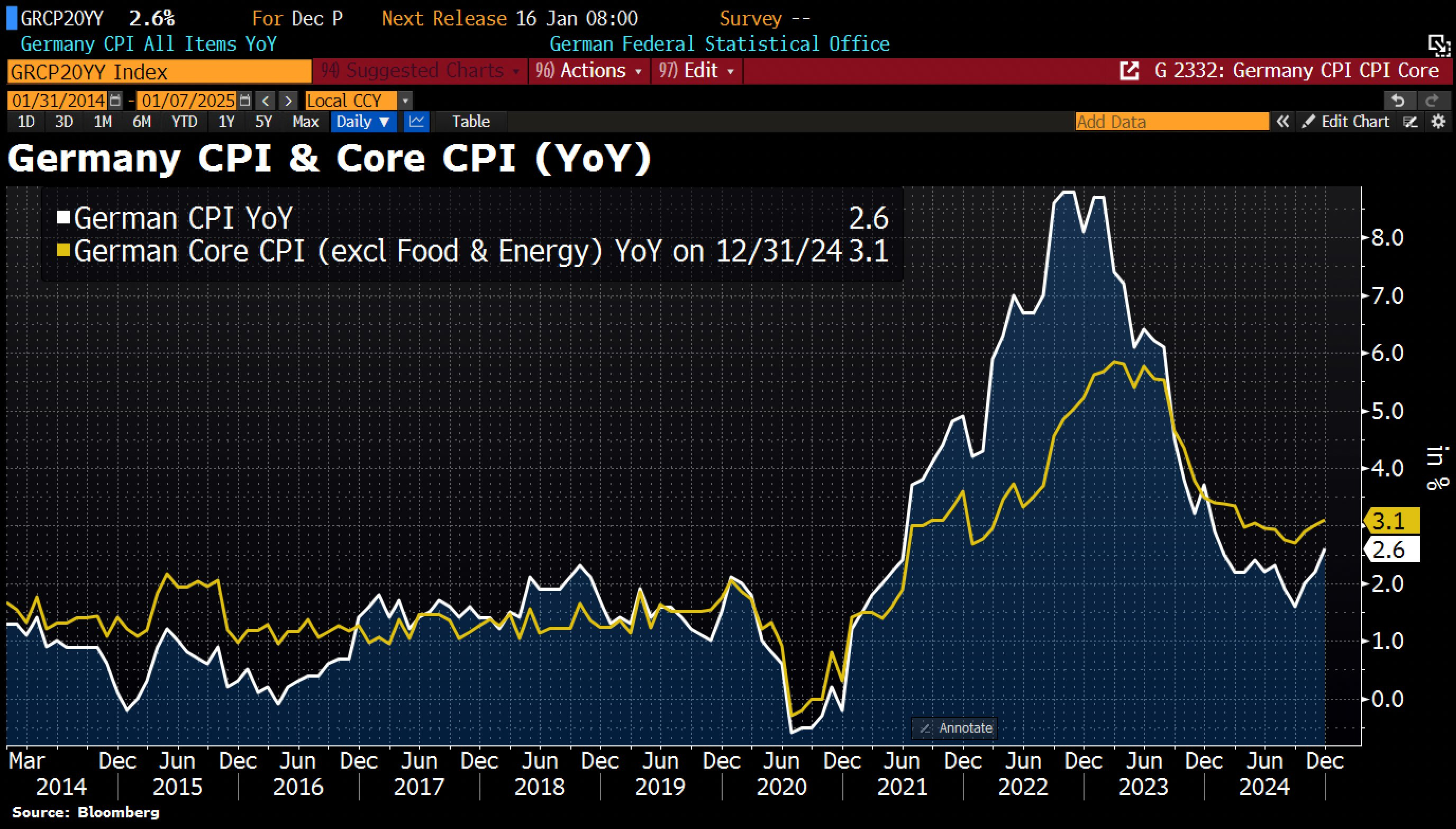

In parallel with this world slowdown, inflation is on the rise once more. The harmonized EU inflation fee in Germany rose to 2.9% year-on-year in December 2022, its highest stage since January and above market expectations of two.4%, in response to preliminary estimates.

Month-on-month, harmonized client costs rose by 0.7%, exceeding forecasts of a 0.5% improve:

The “Core CPI” index, which excludes the Vitality and Meals classes, as soon as once more exceeded 3%:

Inflation picked up throughout the European continent in December:

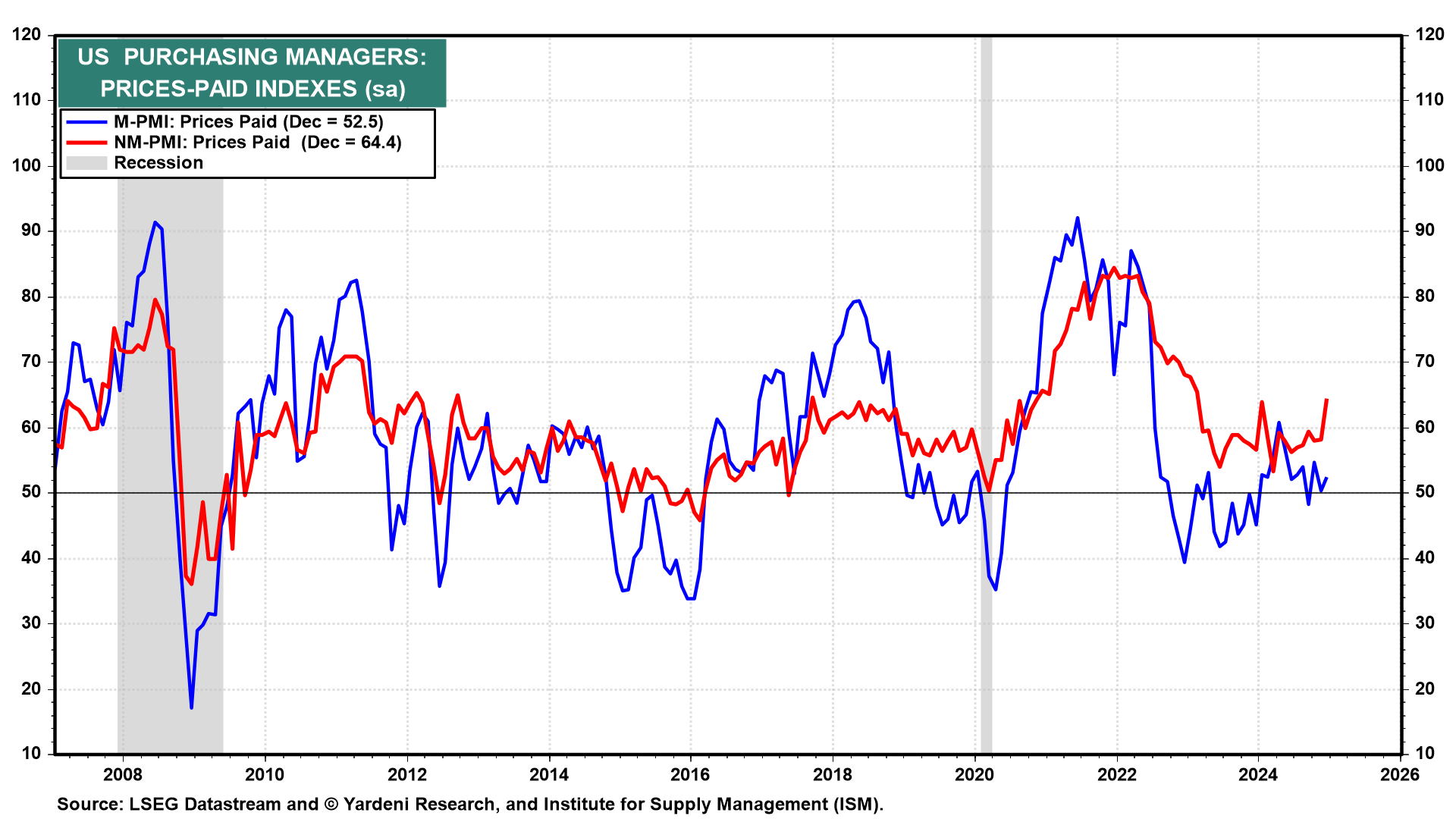

In america, inflation figures are additionally rising: the paid value index has reached 64.4, in contrast with a forecast of 57.5 and a earlier studying of 58.2:

Is that this renewed inflation behind the rise in charges?

The yr 2025 is off to a really dangerous begin for the sovereign debt market.

The British 10-year GILT has returned to its lowest ranges:

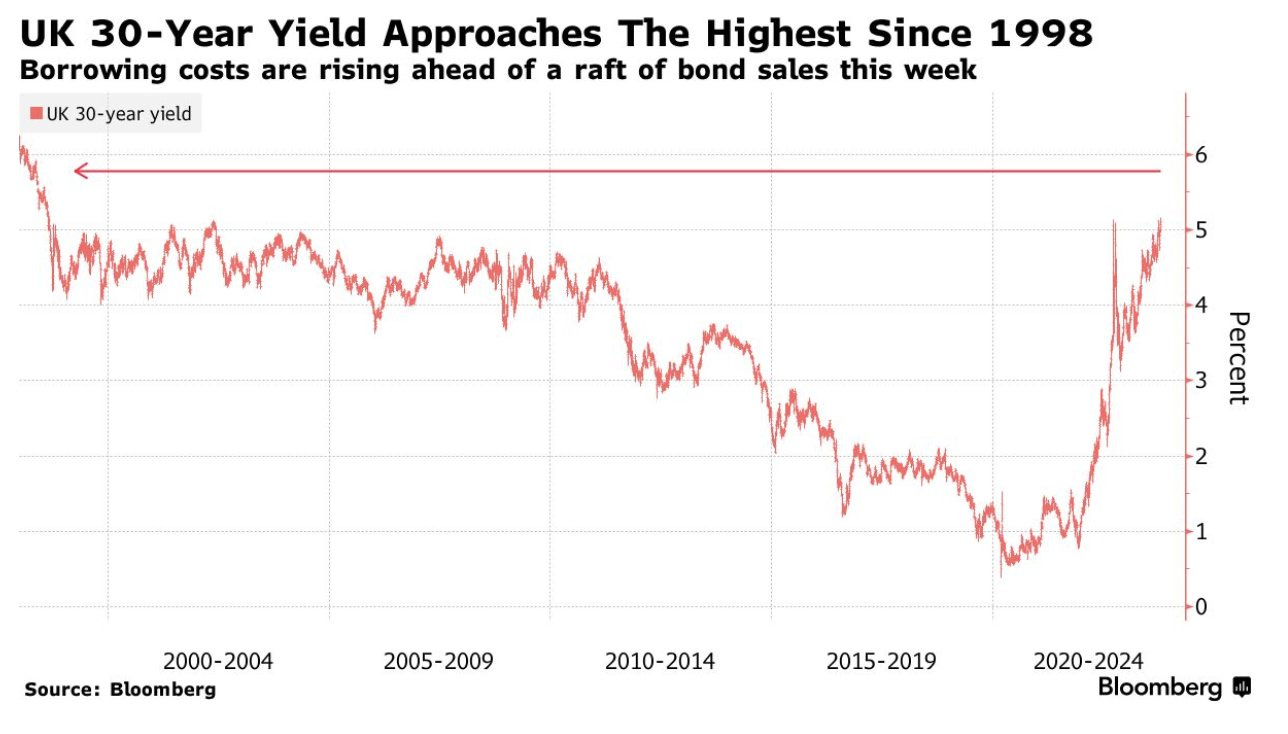

UK 30-year yields are again to their highest ranges since 1998:

The identical stage of charges had beforehand led to intervention by the Financial institution of England.

In 2023, the Financial institution of England needed to intervene urgently when rates of interest reached a essential stage, creating tensions on monetary markets. The primary intention of this intervention was to stabilize bond yields and forestall a systemic disaster, by supporting weakened gamers reminiscent of pension funds, already affected by the fast rise in rates of interest. The state of affairs was paying homage to the 2022 disaster linked to LDI methods, when extreme volatility jeopardized market liquidity and the economic system.

Are we as soon as once more on the verge of intervention by the Financial institution of England?

US charges are additionally climbing to report ranges in the beginning of the yr:

The autumn within the bond market is accelerating, with the TLT index breaking a brand new bear flag within the first few periods of the yr:

The French bond market has additionally been underneath strain for the reason that begin of the yr. 10-year yields are approaching 4%, apparently signalling the top of the low-rate period that has dominated France for the reason that 2000s:

The decline within the bond market is pushing fairness markets to new heights. Evidently the “Magnificent 7” at the moment are seen as a secure haven from bond market dangers. Not so way back, the bond market was seen as a refuge from market uncertainties, however as we speak, the state of affairs has been reversed!

The Nasdaq is sustaining its beneficial properties after two years of spectacular will increase:

People are notably eager to purchase equities in the beginning of the yr, with expectations of excessive development within the retail market:

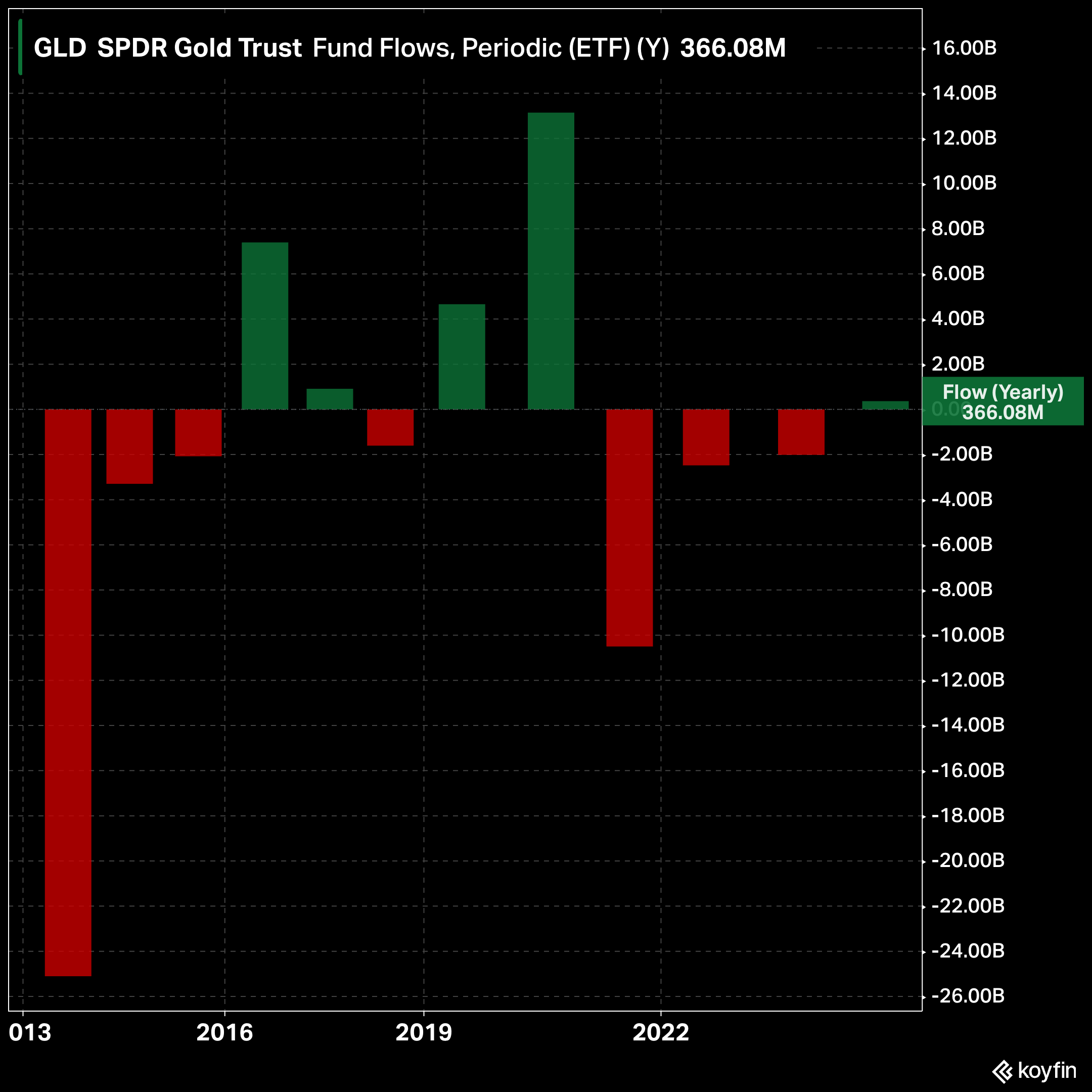

The onset of a worldwide recession, the persevering with collapse of the bond market in early 2025, and the dangers it poses to the banking sector and the economic system as an entire, are the principle causes presently underpinning the rise in gold costs.

Neither rising rates of interest nor a robust greenback have succeeded in driving gold down for lengthy. Quite the opposite, the valuable metallic is changing into much more enticing to Western traders.

The rise within the GLD fund’s property underneath administration in latest weeks marked the top of a interval of outflows that had lasted since 2022. For the primary time in 4 years, GLD has recorded constructive internet inflows, testifying to the return of Western traders to gold in latest weeks:

Replica, in complete or partially, is permitted so long as it contains all of the textual content hyperlinks and a hyperlink again to the unique supply.

The data contained on this article is for info functions solely and doesn’t represent funding recommendation or a advice to purchase or promote.