In my bulletin from January 19, 2024, titled “The Fed Has Not Received the Struggle on Inflation”, I wrote: “The resurgence of inflation will definitely complicate the Fed’s process relating to making the choice that markets have been anticipating for a number of weeks: inventory market efficiency is defined solely by the Fed’s promise of a fee lower.”

I had additionally added: “Total, the market doesn’t appear to be taking up board the danger of provide disruptions in uncooked supplies. But this threat is likely one of the key components that might radically alter the inflation image.”

Twelve months on, the danger of disruption stays largely absent from valuations, and commodity costs, with a number of exceptions, have remained surprisingly depreciated all through 2024.

Agricultural commodities comparable to espresso, orange juice, chocolate, and eggs have risen spectacularly in latest months, primarily as a consequence of components particular to those markets, comparable to drought or avian flu. Metals, alternatively, haven’t carried out remarkably effectively this yr, with buyers seemingly ruling out the opportunity of short-term shortages.

So far as metals are involved, buyers appear to be largely ignoring the danger of shortages… till they develop into a actuality, as was the case in 2024 for germanium, gallium and, extra just lately, antimony:

China has the flexibility to trigger steel costs to fluctuate, if solely by deciding to ban exports. Because it controls the processing of nearly all metals, it exposes these markets to a major threat of value spikes, notably within the context of a commerce warfare. In the interim, this threat stays largely underestimated by the markets. For instance, copper closes 2024 on the similar degree as at the beginning of the yr:

Copper has even misplaced one greenback since its June highs.

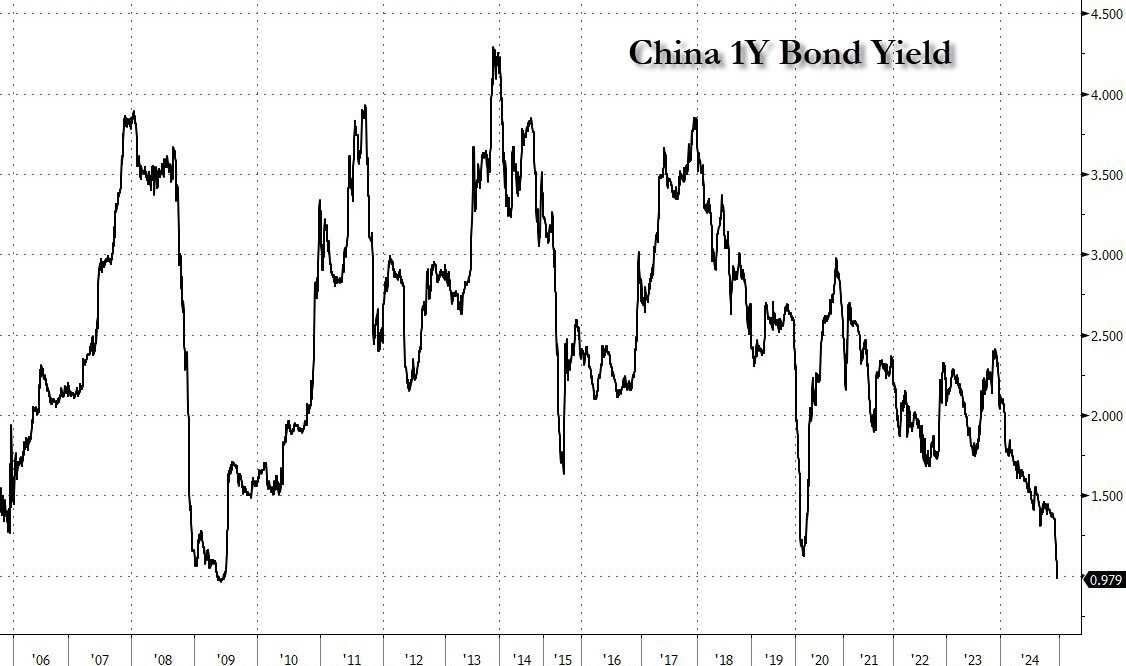

Futures sellers are anticipating a sharper-than-expected slowdown in China. These bearish speculators are influenced by the evolution of Chinese language bond yields.

China’s 1-year yields have collapsed this yr, reaching ranges corresponding to these seen through the nice monetary disaster of 2008. They’ve even fallen under the values recorded through the Covid disaster in 2020:

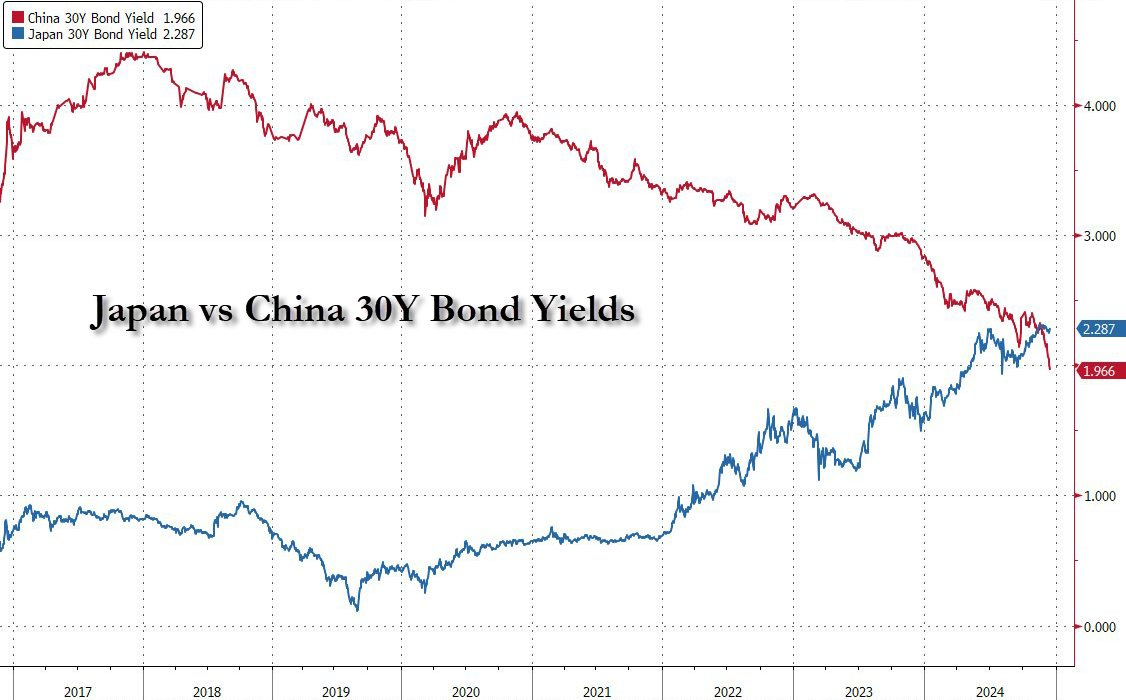

The Chinese language 30-year has simply fallen under the Japanese 30-year for the very first time:

Keep in mind that in 2014, the Chinese language 30-year was at 5%:

The Japanese 30-year was 0% in 2016:

In my bulletin from February 9, 2024 entitled “China: The Deleveraging Course of Has Begun”, I had written: “The actual property sector accounts for 1 / 4 of China’s GDP, however excessive ranges of leverage recommend that the sector’s deleveraging course of may ship many banks right into a deflationary spiral.

In response to analyst Kyle Bass, who is sort of essential of China, there may be even a wider systemic threat inside the Chinese language monetary system and financial system, related to the colossal debt of the nation’s actual property sector”.

As 2024 attracts to a detailed, buyers stay satisfied that China is following a “Japanization” trajectory, characterised by an imminent demographic collapse and chronic dangers in the actual property and banking sectors. These challenges may require an enormous “Japanese-style” help package deal within the years forward.

These issues about China are in all probability behind the rise in gold ETF outstandings this yr.

In my bulletin from April 9, titled “Gold ETF Rush in China”, I offered this chart of China’s hottest gold ETF:

Eight months later, ETF property beneath administration proceed to soar:

The scenario is totally totally different within the USA, the place progress prospects in 2024 have by no means been unsure. The energy of the US financial system, supported by huge authorities spending plans and considerable liquidity, has even led to an actual consciousness of inflation.

In early March, Janet Yellen, the US Treasury Secretary, shocked the markets by admitting that she regretted having described inflation as “transitory”.

In Europe, inflation in 2024 is all of the extra worrying as it’s accompanied by a marked financial slowdown.

In my February 2, 2024 bulletin titled “Europe Paralyzed by First Inflationary Shock”, I had written: “Current rises in inflation have plunged the continent into an unprecedented stalemate: the farmers’ protest motion is especially attributable to the implications of this normal decline in buying energy noticed in Europe over latest quarters. Nevertheless, in keeping with Brussels, one of many options to counter inflation additionally entails negotiating free-trade agreements to include the rise in costs of agricultural uncooked supplies. However these agreements are extremely unfavorable to farmers, who’ve already seen their actual wages plummet in 2022 and 2023. The anti-inflationary remedy is worse than the illness! Prior to now, open borders had been an efficient recipe for holding value rises. Nevertheless, now that inflation has woken up, this strategy now not works.”

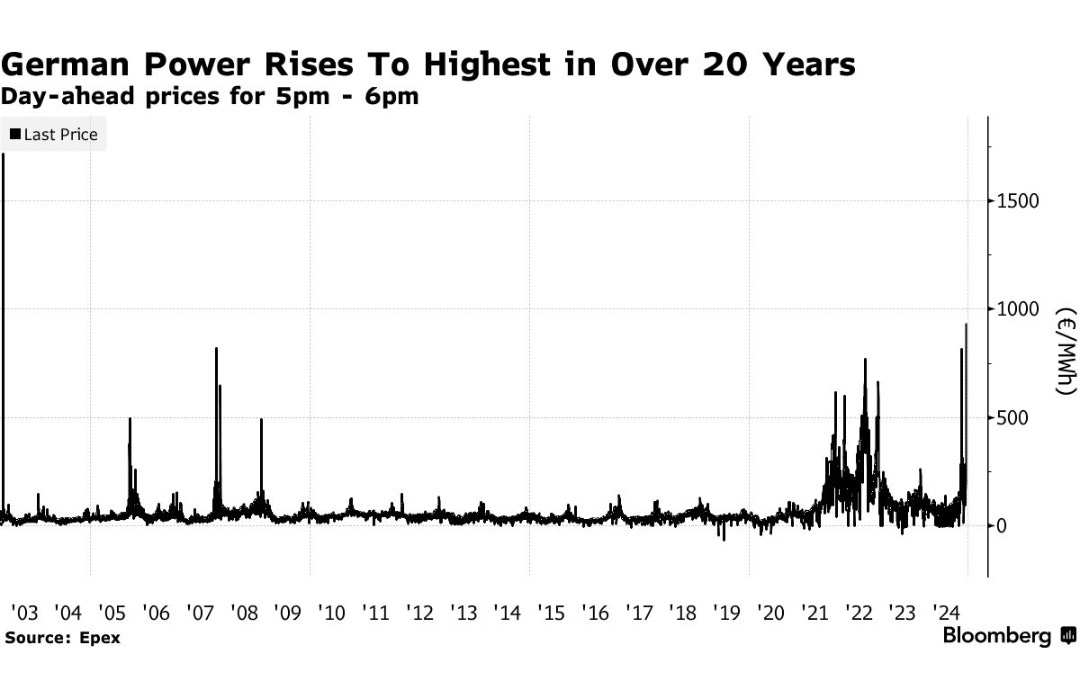

Eleven months after the farmers’ revolt in Europe, nothing has been resolved concerning inflation and the causes of hovering power prices on the continent.

Electrical energy costs in Germany have risen sharply in latest days, reaching ranges not seen for the reason that 2022 power disaster, as a consequence of low wind energy manufacturing. On Wednesday, electrical energy imports reached their highest degree in a decade, forcing fuel and oil-fired energy vegetation to step in to fulfill demand. Costs exceeded €1,000 per megawatt-hour and stay extraordinarily excessive:

Stagflation is about to take maintain in Europe in 2024, however paradoxically, European savers are nonetheless very passive within the face of the danger posed by the specter of this coming interval of stagflation to the worth of bond property held by savers and to the solvency of the French banking system.

In the US, the danger of inflation additionally intensified because the yr drew to a detailed. The newest PPI figures affirm this rebound in inflation. Consequently, with inflationary expectations on the rise, it is just logical that 10-year yields ought to as soon as once more soar to new highs. Regardless of the Fed’s fee lower in September, charges have returned to their highest degree since Could:

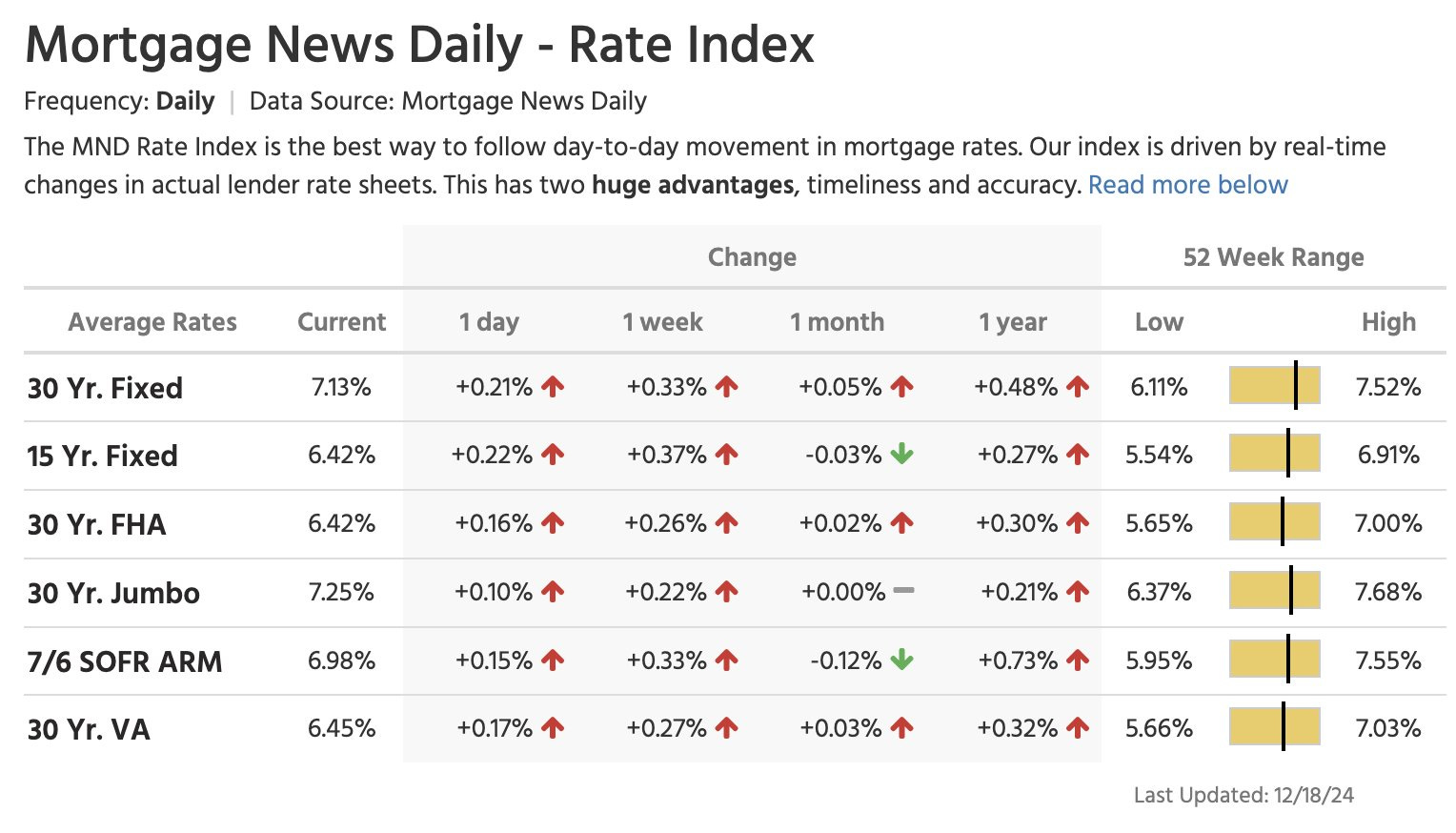

As a direct consequence, the US actual property market is as soon as once more beneath stress.

Final July, I stated that the actual property market was paralyzed by excessive rates of interest. The scenario is deteriorating once more: the typical 30-year mortgage fee rose sharply to 7.13% after the Fed’s press convention, in contrast with 6.65% on the similar time final yr:

These excessive charges additionally signify an enormous problem for short-term refinancing of US debt.

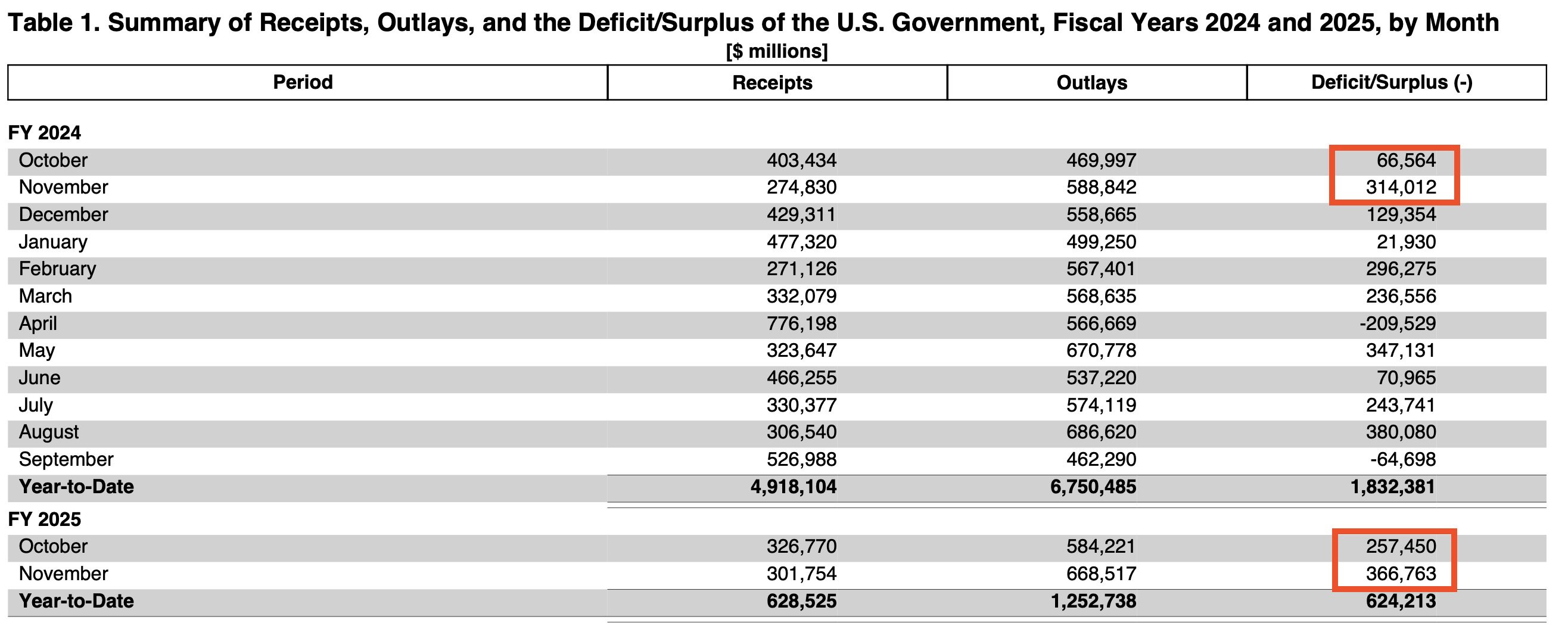

This problem is all of the extra colossal because the deficit continues to develop at an alarming fee. Within the first two months of fiscal 2024, the whole deficit reached $380.5 billion, a scenario that’s already worrying. However over the identical interval of fiscal 2025, this determine soared to $624.2 billion, a spectacular 64% enhance in only one yr!

A rising proportion of debt is now financed by short-term payments maturing in lower than a yr. With $2 trillion in bonds, notes and payments maturing in 2025, plus one other $2 trillion in annual price range deficits (and nonetheless this determine is prone to be far exceeded), gross financing necessities attain a complete of $4 trillion.

The necessity to finance such a lot of new debt is the principle argument in help of the forecast enhance of the value of gold in 2025.

Replica, in complete or partially, is allowed so long as it contains all of the textual content hyperlinks and a hyperlink again to the unique supply.

The data contained on this article is for info functions solely and doesn’t represent funding recommendation or a advice to purchase or promote.