The US actual property market is experiencing an unprecedented freeze. Mortgage demand within the US has fallen to its lowest stage since 1995. In lower than 4 years, mortgage purposes have fallen by a spectacular 63%, reflecting rising purchaser disaffection:

Taxes and insurance coverage: a rising burden

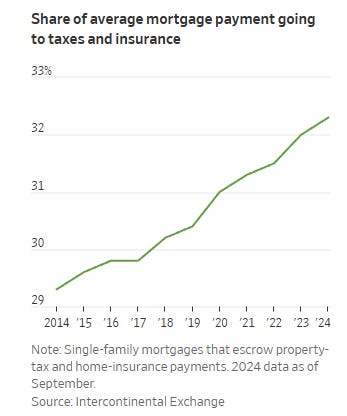

In September, a report 32% of US family mortgage funds have been absorbed by taxes and insurance coverage, decreasing the margin accessible for principal compensation:

This phenomenon is especially pronounced in areas similar to Miami and Rochester, the place these bills now account for greater than half of month-to-month funds. A living proof is a household in New Orleans, whose tax and insurance coverage bills have risen from $725 to $2,448 per 30 days, exceeding even their month-to-month mortgage fee. On this context, some owners are foregoing insurance coverage, as is the case for 21% of house owners in Miami, whereas others are contemplating shifting to states the place life is inexpensive.

This example highlights a structural disaster in actual property financing, amplified by rising prices linked to local weather change and regulatory necessities.

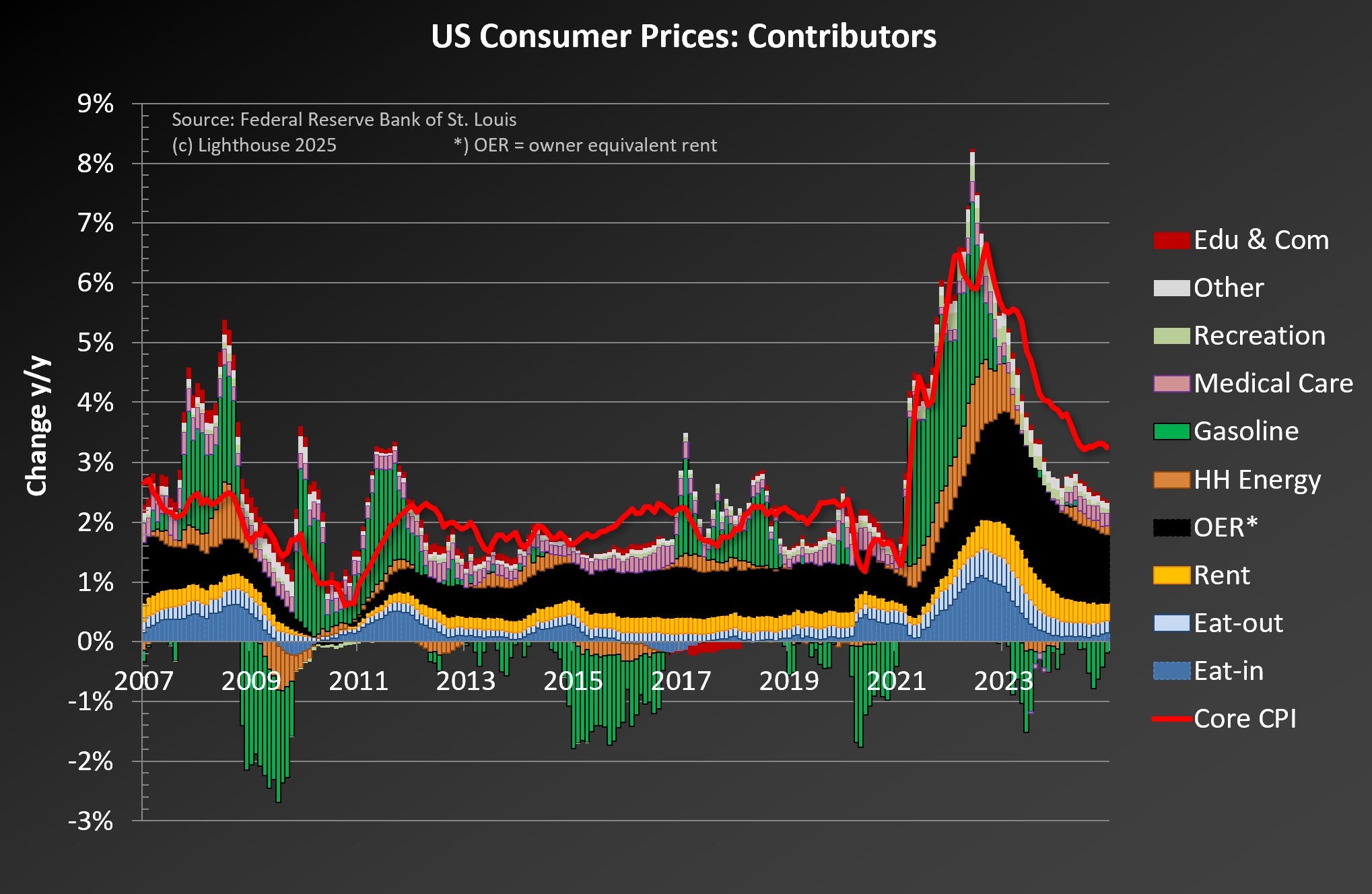

Housing – each rents and property bills – has turn out to be the principle driver of US inflation, overtaking objects similar to vitality and gasoline. With mortgage funds accounting for a better proportion of median revenue than in 2006, the scenario is unlikely to enhance:

Inflation is now specializing in the prices related to property upkeep, whereas public establishments, closely in debt, are elevating taxes to alleviate their money owed. Consequently, housing shouldn’t be solely turning into increasingly costly to amass, but in addition increasingly costly to personal!

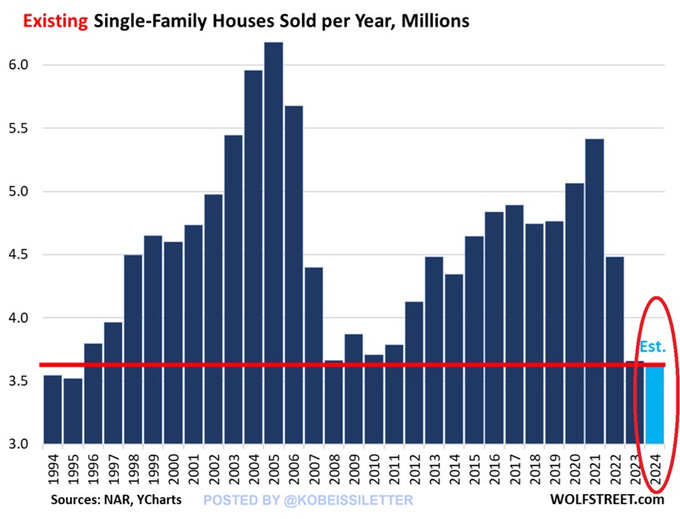

A stalled market, gross sales at an all-time low

In 2024, gross sales of present properties fell to their lowest stage since 1995, with round 4.04 million transactions, a determine even decrease than that seen throughout the 2008 disaster:

A no-win scenario for a lot of owners

In 2024, an alarming phenomenon emerged: shopping for a brand new residence has turn out to be inexpensive than shopping for an present one! On common, a brand new residence prices $417,400, in contrast with $419,300 for an present residence. An anomaly that illustrates the market’s important scenario.

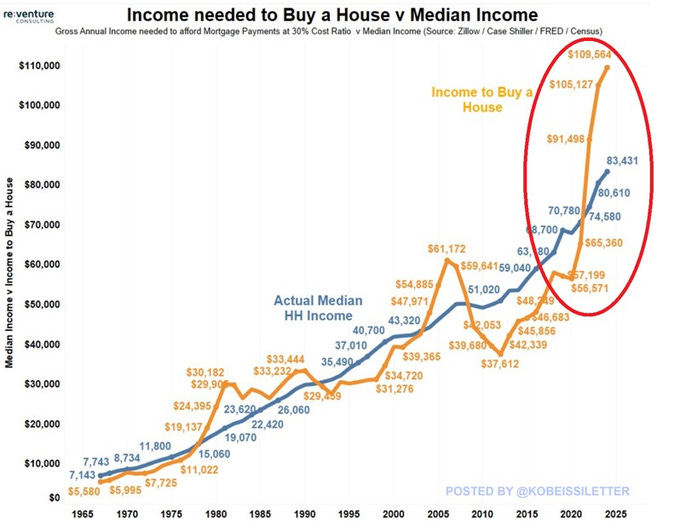

Unaffordable housing for many households

The flexibility to personal a house is reaching important ranges. The annual revenue required to purchase a median-value residence has reached a report $109,564, a determine that has doubled in simply 4 years. By comparability, the median family revenue within the U.S. presently stands at $83,431, a spot of $26,133:

The flexibility of American households to entry residence possession has by no means been so low.

The market is totally frozen, and this paralysis is the results of a formidable mixture: excessive rates of interest and report costs. The common age of residence consumers is now 49, in contrast with 31 in 1981, illustrating the rising hole between youthful generations and residential possession.

Younger folks’s disaffection with property purchases is mirrored in a marked shift in the direction of different sorts of funding.

In my December bulletin, I wrote that the push into crypto-currencies primarily issues youthful buyers, notably Technology Z, for whom conventional funding, similar to energetic administration and hedge funds, is a factor of the previous. At this time, they favor high-potential methods with asymmetrical danger (restricted losses, exponential beneficial properties). This craze can also be the logical consequence of the youthful era’s lack of ability to entry property possession. The American dream appears laborious to realize, fully altering the way in which folks take into consideration investing.

Confronted with prohibitive prices, plummeting gross sales and crushing encumbrances, the U.S. actual property market has reached an deadlock.

With out important intervention, residence possession might turn out to be an much more distant dream for thousands and thousands of People.

The hazard lies within the potential detour of a whole era from such a funding. What’s extra, some US establishments may very well be laborious hit by a collapse in the actual property market.

In February 2024, I wrote in a particular bulletin that the actual property sector accounted for 1 / 4 of China’s GDP, and excessive ranges of leverage led to fears that the deleveraging of the sector might ship many banks right into a deflationary spiral.

The rise within the value of gold in 2024 is especially because of the actual property disaster in China. Many buyers, beforehand targeted on actual property, have redirected their capital into gold. Furthermore, the worry that the collapse of the Chinese language actual property market might have an effect on the banking sector has prompted many savers to show to this protected haven par excellence. Gold is thus positioned because the final bastion in opposition to a doable systemic banking shock or foreign money devaluation ensuing from a Chinese language rescue plan to prop up its banks.

China’s actual property disaster has propelled demand for bodily gold to report ranges. It’s exactly this robust bodily demand that explains the current spectacular rise within the value of gold.

The worth of gold in renminbi has virtually doubled within the area of two years:

At this time, the scenario within the US presents comparable dangers, with the actual property sector at an entire standstill. Confronted with this paralysis and the uncertainties it engenders, bodily gold now performs the identical position in america because it did in China final 12 months: a protected different within the face of financial and monetary instability.

Replica, in entire or partially, is allowed so long as it contains all of the textual content hyperlinks and a hyperlink again to the unique supply.

The data contained on this article is for info functions solely and doesn’t represent funding recommendation or a advice to purchase or promote.