France, Italy, Japan and the USA all have excessive finances deficits of comparable magnitude, accompanied by important public debt in extra of 100% of GDP. Nevertheless, taking a step again and integrating different macroeconomic monetary information, threat ranges differ drastically, to France’s detriment. That is what a current article by Patrick Artus, which takes into consideration all capital actions affecting these nations, signifies.

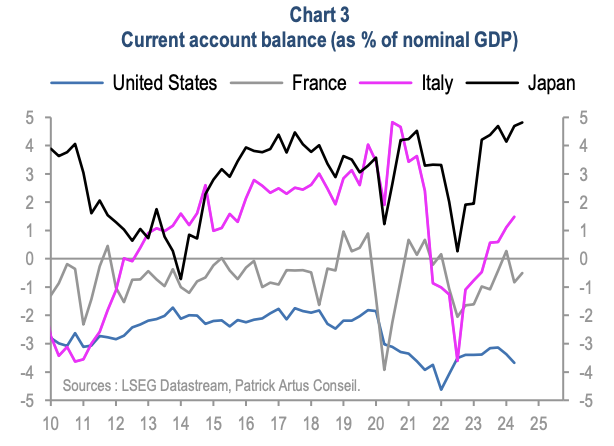

Let us take a look at the present account steadiness, which totals the commerce steadiness (trade of products and companies with overseas nations) and the revenue steadiness (from investments overseas or paid to foreigners who’ve invested within the nation, salaries paid or acquired from overseas). France and america are within the purple, however Japan and Italy are structurally in surplus, which allows them to finance their deficits comparatively simply, and that is mirrored in a public debt that’s primarily held by nationwide financial savings (over 90% in Japan, 80% in Italy). As exterior constraints are low, overseas investor mistrust would don’t have any main impression.

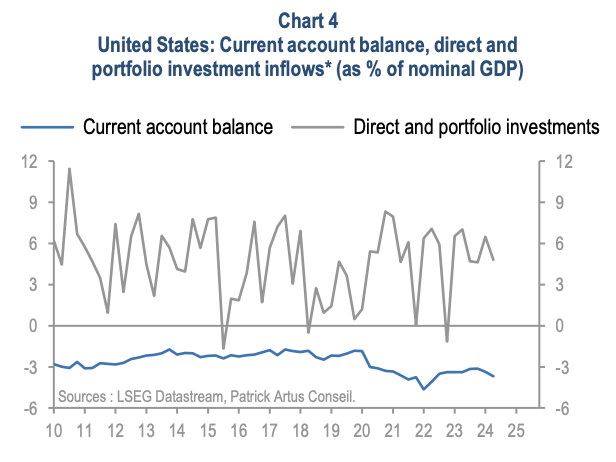

America, then again, advantages from substantial inflows of long-term capital. That is the product of their financial attractiveness, whether or not in expertise, capital administration (monetary markets, hedge funds), industrial renewal (low-cost vitality, IRA program), or the safety supplied by the world’s main energy. Financing the big public debt ($36 trillion) can be comparatively simple (23% held by non-residents). Not forgetting, in fact, the greenback’s inescapable function as a transaction and reserve foreign money, which obliges the world’s nations to inevitably maintain it.

France, then again, doesn’t offset its recurrent finances deficit with a constructive present account steadiness, and even suffers – the article does not point out it, however we pointed it out in our earlier article- a worrying outflow of capital.

France subsequently scores all of the incorrect factors, as may be seen from the truth that non-residents, i.e. overseas traders, maintain 54% of its public debt, far larger than the opposite nations talked about.

As Patrick Artus factors out, “Essentially the most harmful case: nations with a finances deficit, a present account deficit and no long-term capital inflows.”

| France | Italy | Japan | United States | |

| Public deficit | – | – | – | – |

| Present account steadiness | – | + | + | – |

| Lengthy-term capital inflows/outflows | – | 0 | 0 | + |

(-: deficit; +: surplus; 0: steadiness)

Please be aware that we aren’t saying {that a} excessive finances deficit just isn’t severe, however that the pressure it locations on a rustic is determined by its general capital flows. And for France, the state of affairs is especially harmful: a lack of confidence on the a part of overseas traders might quickly result in an incapability to finance, resulting in a collapse of the monetary system, adopted by a freeze on financial institution accounts and life insurance coverage (BRRD directive and Sapin II Legislation, see our earlier article).

After we see the futility of the 2025 finances, the inconsistency of the debates, the lack to cut back spending, the Lépine competitors to create new taxes, we are able to solely conclude that this sword of Damocles is clearly not taken into consideration by the political workers.

Let’s hope savers aren’t blind both…

Copy, in complete or partially, is allowed so long as it contains all of the textual content hyperlinks and a hyperlink again to the unique supply.

The knowledge contained on this article is for data functions solely and doesn’t represent funding recommendation or a advice to purchase or promote.