A yr in the past, I wrote that bodily gold had grow to be a extra dependable possibility than Treasury Payments.

Central banks’ shopping for frenzy has strengthened gold’s standing as a reserve asset. In keeping with Financial institution of America, gold has now overtaken the euro to grow to be the world’s second largest reserve asset, after the US greenback, accounting for 16% of the reserve pool.

How did T-Payments handle to lose their historic standing as a safe-haven asset in portfolios to such an extent?

The World Gold Council just lately revealed an article explaining why, by 2024, gold is ready to grow to be the last word defensive asset, changing bond belongings.

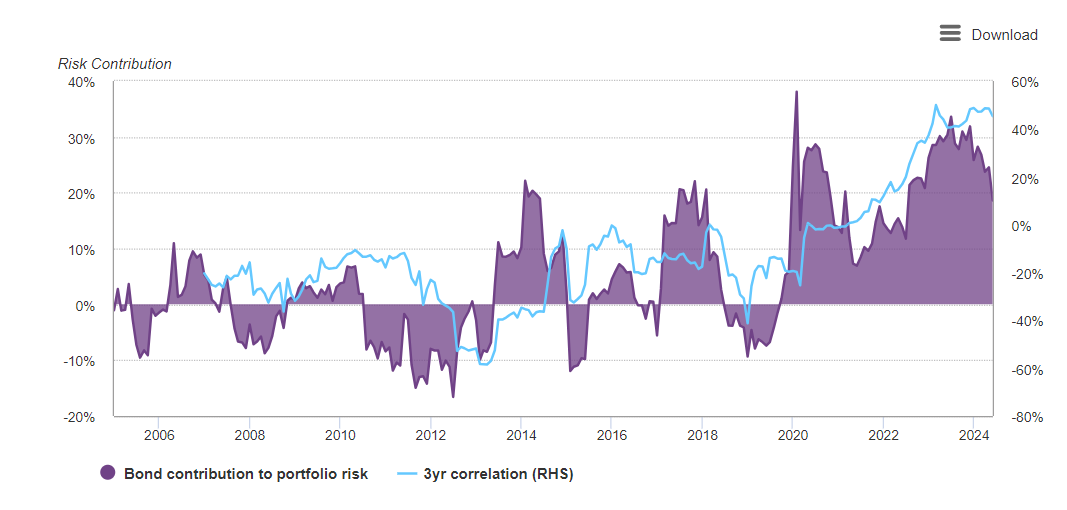

The research’s most important chart, revealed on web page 3, illustrates the chance contribution of the 2 asset courses, equities and bonds:

The purple a part of the chart reveals the contribution of bonds to whole portfolio danger, expressed as a share. There was a marked improve on this contribution over time, particularly after 2014, with vital peaks round 2020 and 2023, reaching nearly 40%. The contribution of bonds to danger has fluctuated considerably in recent times, with a number of durations of detrimental contribution (i.e., bonds lowering total portfolio danger) previous to 2014.

In recent times, the general development has been upwards, indicating that bonds have gotten an more and more essential supply of danger. Not solely do they now not shield portfolios, additionally they improve total danger!

The blue line reveals the three-year correlation between bonds and Swiss equities. This correlation, represented on the right-hand axis, oscillates between detrimental and constructive values. When the correlation is detrimental, it implies that bonds and equities are shifting in reverse instructions, which, in principle, ought to cut back total portfolio danger.

In recent times, nevertheless, correlation has grow to be constructive. A constructive correlation implies that bonds and equities are shifting in the identical route, thereby rising total portfolio danger.

A 60/40 portfolio now not mitigates the chance of market publicity; quite the opposite, it reinforces it.

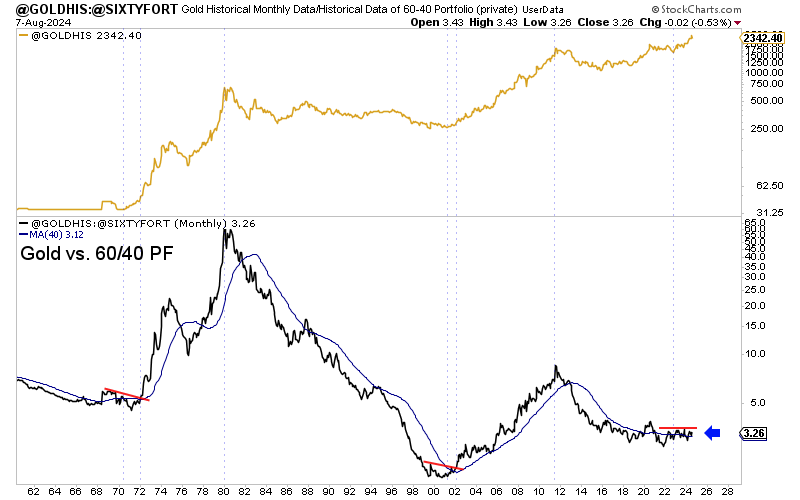

Gold is at the moment outperforming the 60/40 portfolio, at a time when traders are waking as much as this actuality. As I defined two weeks in the past, gold is breaking by means of an essential restrict in contrast with the “basic” 60/40 portfolio:

Disaffection with Treasuries will also be defined by the conduct of U.S. yields. In 2023, US 10-year bond yields broke with their downward development:

TLT tried a rebound in 2024 on excessive quantity… however the rebound remains to be far too timid:

These sharp breaks within the long-term tendencies of the US Treasury bond market have modified the notion of those belongings. Inflation has modified the face of the US bond market.

Doubts about America’s capability to repay its money owed in a non-devalued forex are rising because the nation sinks deeper into stagflation (an inflationary recession). The Fed appears to be failing in its two mandates. Its battle towards inflation just isn’t received, and it’s doable that the approaching months will see the emergence of a second inflationary wave.

Recession additionally appears to be on the horizon.

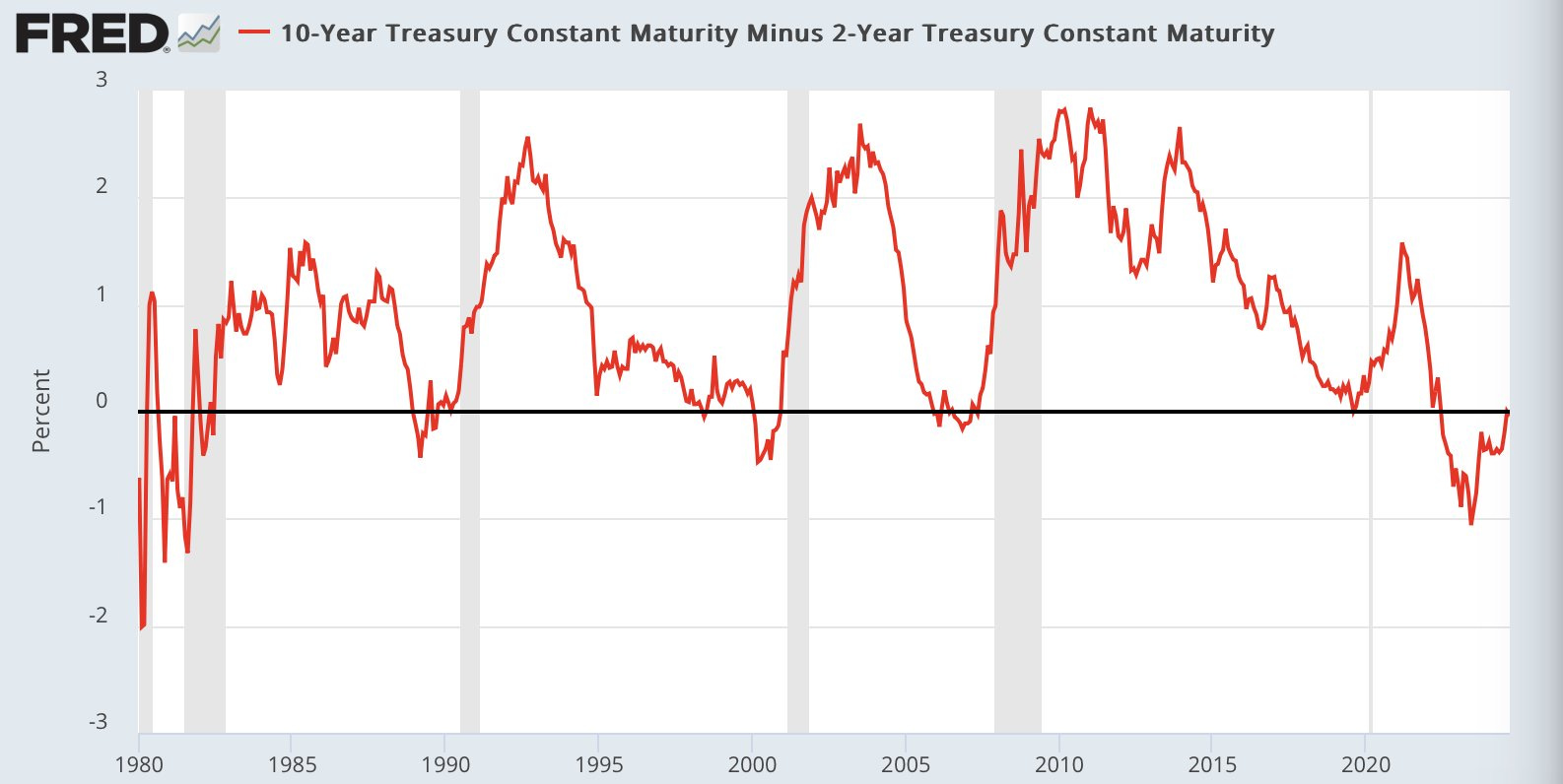

The inversion of the yield curve, an indicator of recession which we now have mentioned many instances in these bulletins, alerts an official entry into recession within the coming weeks:

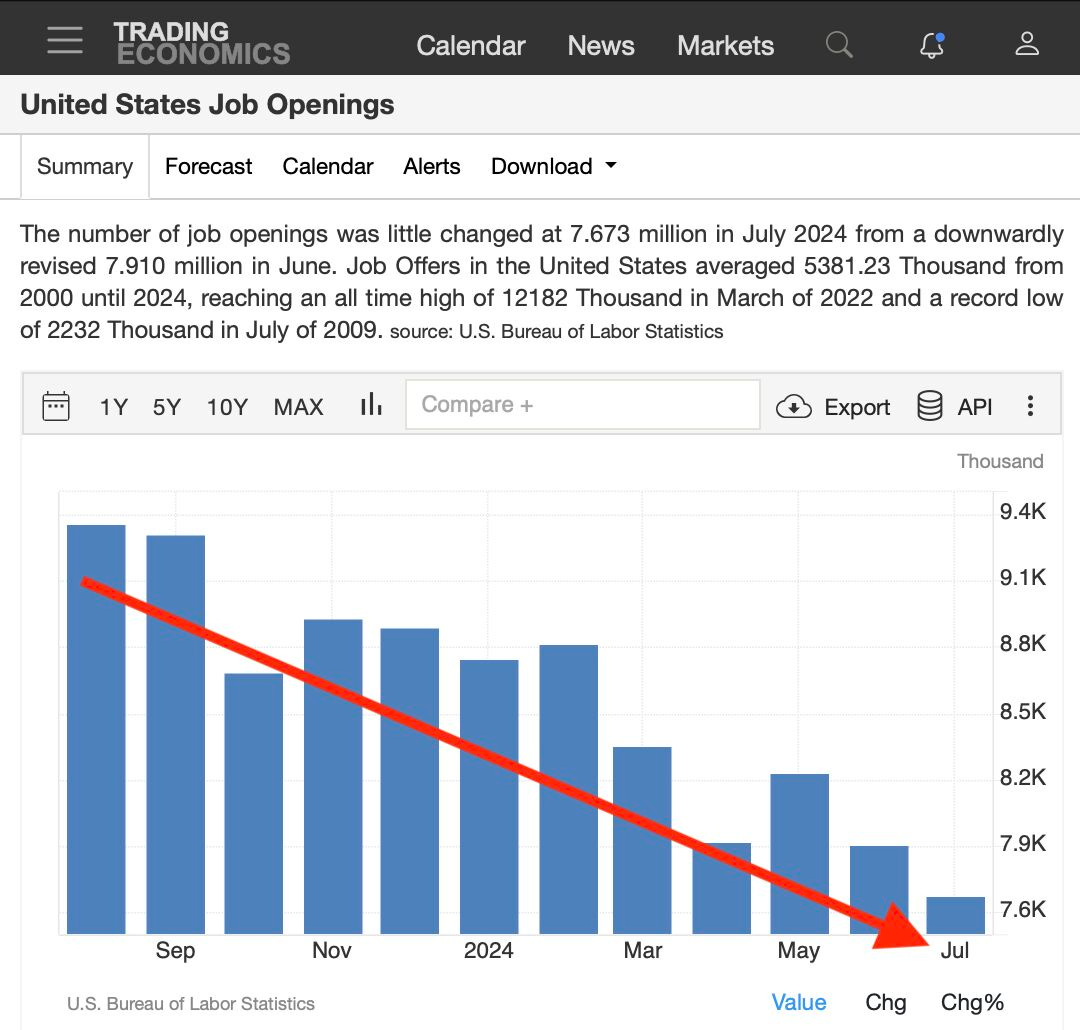

Job openings figures affirm a sharper-than-expected slowdown within the US economic system:

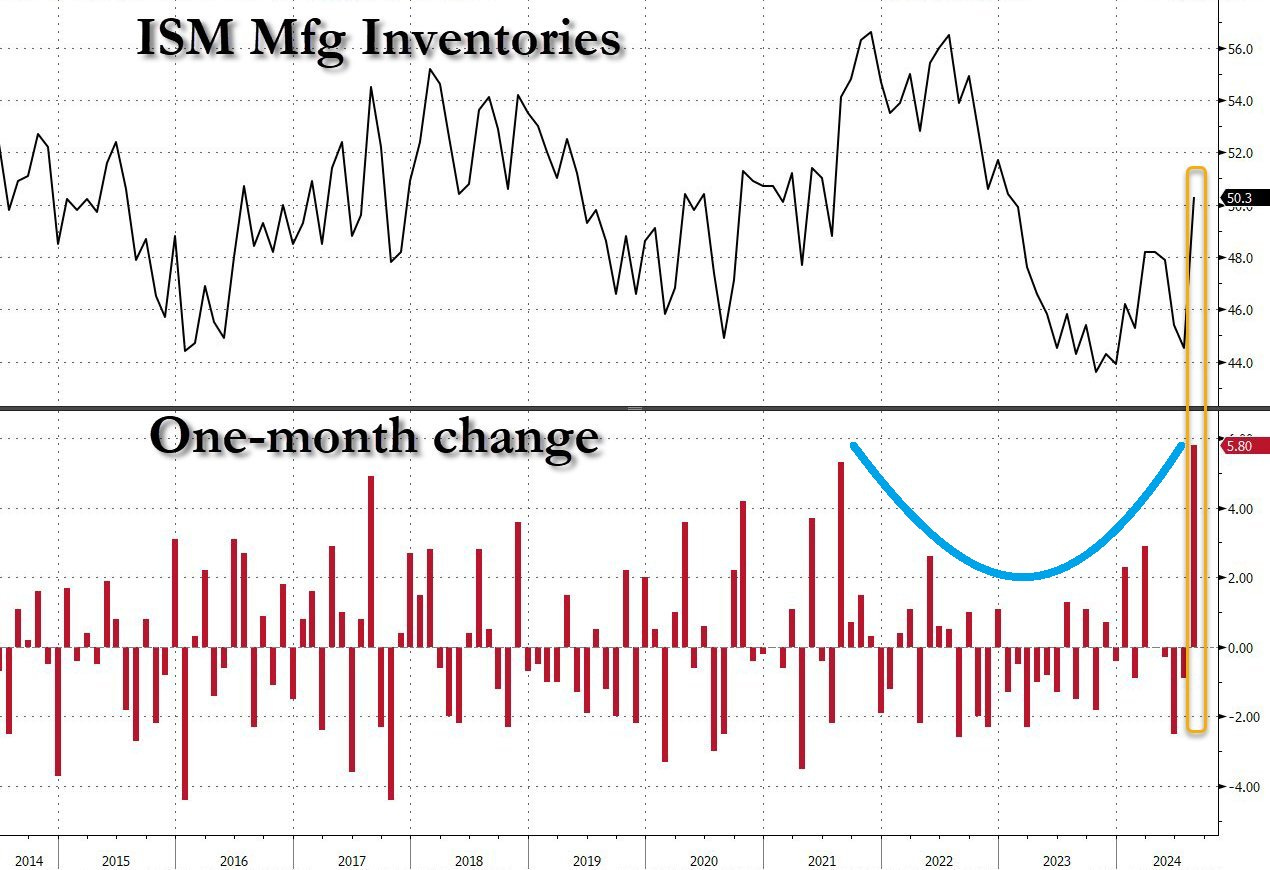

Nevertheless it was above all the newest ISM statistics that despatched the markets right into a frenzy this week.

The US manufacturing sector is now down for the fifth consecutive month, with the index falling to 47.2 factors.

The ISM Manufacturing PMI disillusioned forecasts, which had been anticipating 47.5 factors for final month.

New orders fell to 44.6 factors from 47.4 in July, marking three consecutive months of contraction.

Over the previous 22 months, manufacturing exercise has declined 21 instances, extending the second longest decline in historical past.

Probably the most vital determine amongst these statistics is merchandise inventories:

Inventories have exploded upwards, whereas consumption, the final engine of American progress, is starting to stall abruptly.

What’s notably worrying is that this drop in exercise is now accompanied by a resumption of worth rises. Whereas the rise in inventories ought to theoretically result in a fall in costs, we’re observing the other phenomenon.

The costs paid index climbed to 54 factors from 52.9 in July, the eighth consecutive month of will increase.

Demand has fallen, inventories have risen (attributable to unsold items), and costs have climbed (attributable to labor and transportation prices). That is the very definition of stagflation!

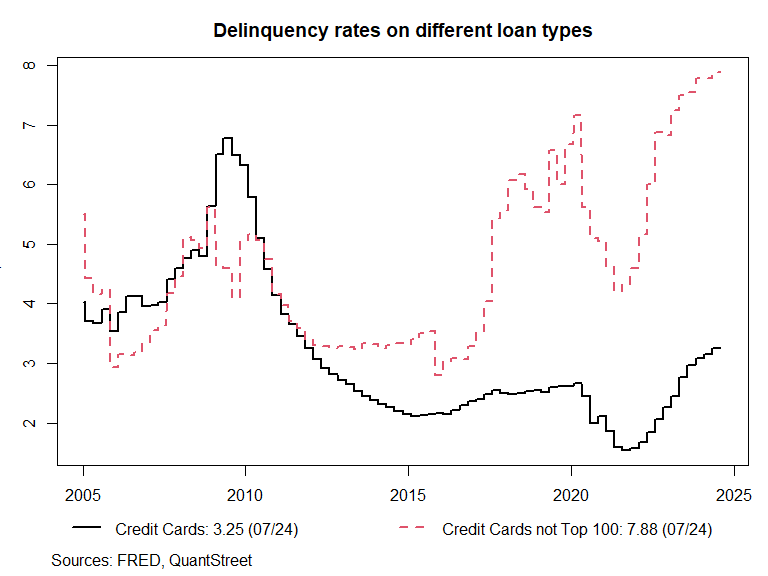

It is the Fed’s nightmare, but additionally that of essentially the most weak customers, who are actually struggling to repay their money owed:

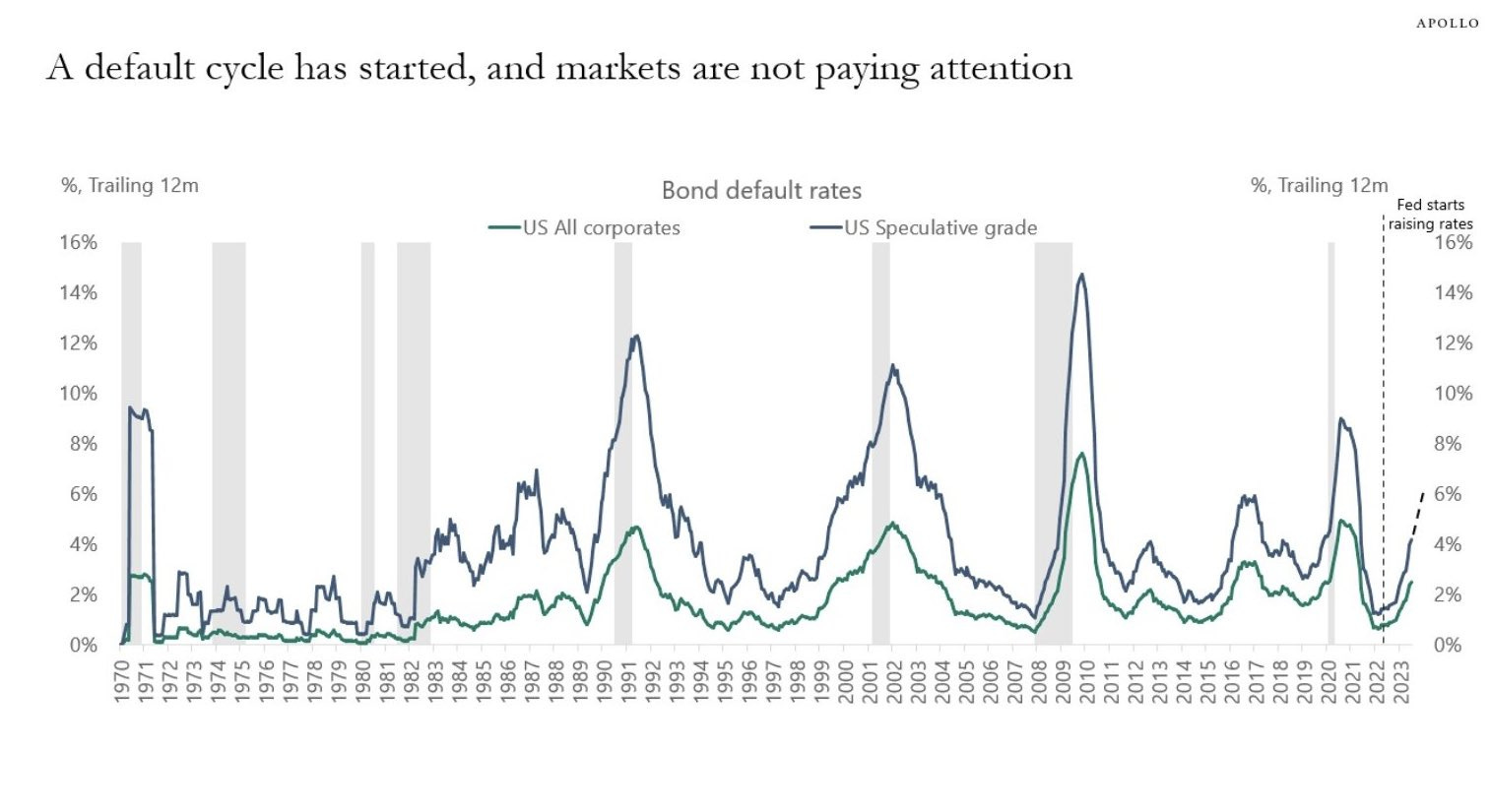

A brand new cycle of defaults has begun in the USA, towards a backdrop of stagflation:

In opposition to this stagflationary backdrop and the beginning of a brand new cycle of defaults in the USA, gold is logically attracting new patrons.

Copy, in entire or partially, is allowed so long as it contains all of the textual content hyperlinks and a hyperlink again to the unique supply.

The knowledge contained on this article is for data functions solely and doesn’t represent funding recommendation or a suggestion to purchase or promote.